Published March 27, 2026

What It Actually Costs to Buy into the Austin Dream in 2026

"Seattle Lateral" vs. The Austin Reality

Meet Elena. A senior project manager from Seattle, Elena received a job offer in Austin’s "Silicon Hills" with a salary of $110,000. On paper, she was ecstatic. In Seattle, $110k barely covers a studio apartment; in Texas—a state famously without income tax—she assumed she would live like royalty.

She sat down with a local Austin lender, expecting to be cleared for a $500,000 home. The lender's response was a sobering "reality check." Because of Austin’s specific property tax landscape and the 2026 interest rate environment, Elena’s $110,000 salary actually placed her slightly below the comfort threshold for a median-priced home.

Elena learned the "Austin Paradox": What you save in state income tax, you often pay back in property taxes and insurance.

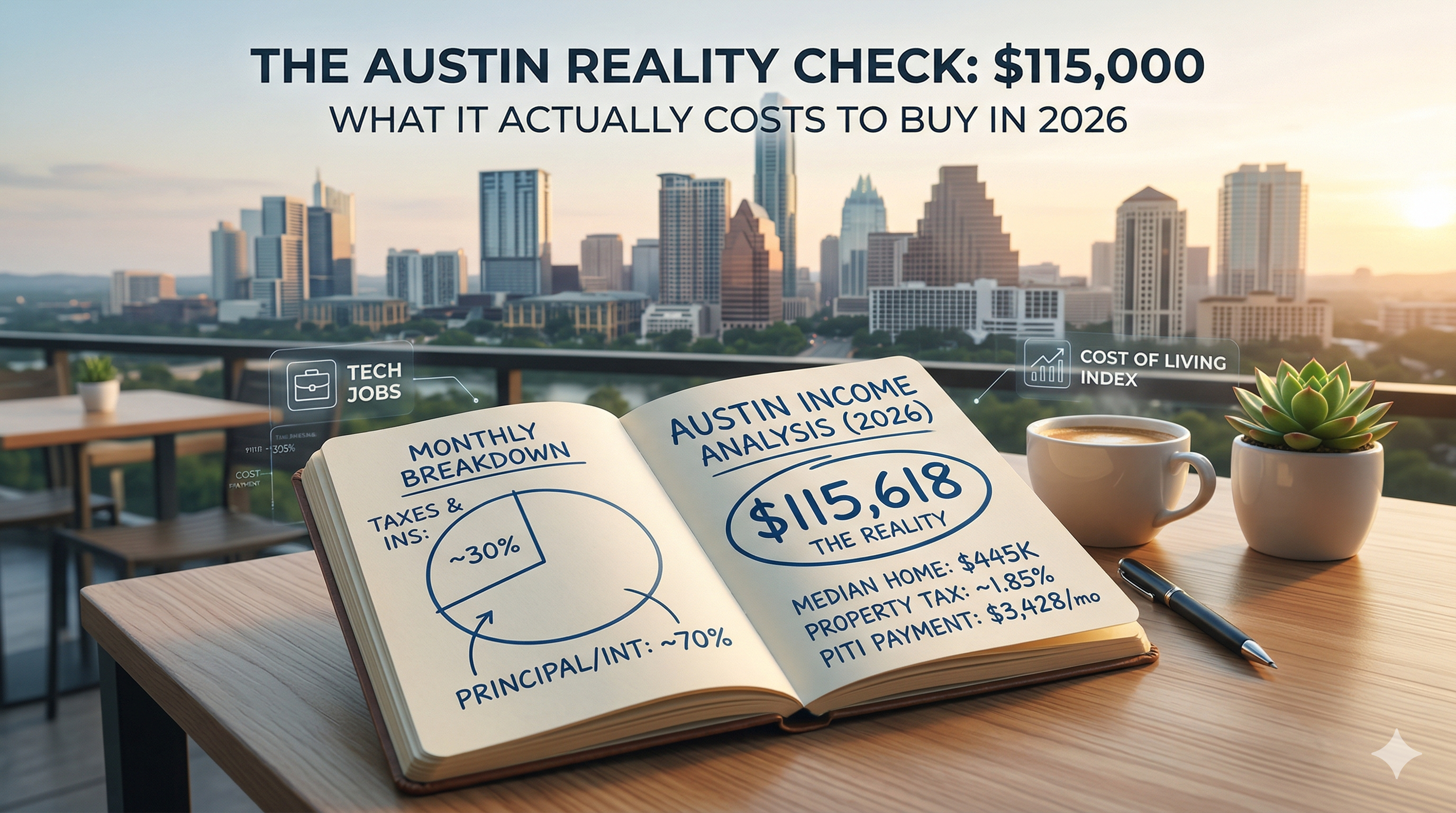

The "Magic Number" for 2026: $115,618

According to March 2026 market data, the annual income required to comfortably afford the median-priced Austin home ($445,000) is exactly $115,618.

This figure isn't just a guess—it's based on the 30% Rule, which suggests that your housing costs (Principal, Interest, Taxes, and Insurance) should not exceed 30% of your gross monthly income.

The Monthly "PITI" Breakdown

If you buy a median-priced home at $445,000 with a 10% down payment and a 6.2% interest rate, your monthly "nut" looks like this:

-

Principal & Interest: $2,453

-

Property Taxes: $685 (Based on a 1.85% average rate)

-

Homeowners Insurance: $180 (Reflecting 2026’s adjusted climate premiums)

-

Private Mortgage Insurance (PMI): $110

-

Total Monthly Payment: $3,428

To pay $3,428 without being "house poor," your gross monthly income needs to be roughly $9,634, which totals $115,618 per year.

Why the "Comfortable" Salary Varies by Neighborhood

Austin is no longer a "one-size-fits-all" city. Your required income changes drastically depending on which side of I-35 you plant your flag.

The 2026 Neighborhood Income Map

| Area | Median Home Price | Income Needed to Buy |

| Central Austin (78701/78704) | $675,000 | $175,000+ |

| East Austin (78702) | $498,000 | $129,000 |

| Pflugerville / Round Rock | $410,000 | $106,000 |

| Southeast Austin (Del Valle) | $358,000 | $92,000 |

| Kyle / Buda | $320,000 | $83,000 |

As the table shows, if you earn $90,000, you are priced out of Central and East Austin, but you are a "strong buyer" in the South Corridor (Kyle/Buda).

The "Hidden" Costs of the Austin Lifestyle

Buying the house is only the first step. To live "comfortably" in 2026—meaning you can still afford a night out on Rainey Street or a pass to ACL Fest—you have to account for Austin's unique cost-of-living quirks:

-

The "AC Tax": Austin summers in 2026 remain brutal. Budget $250–$350/month for utilities (Austin Energy) during the June–September stretch.

-

Transportation: While Austin's public transit has improved, it remains a car-dependent city. Between gas, tolls on the 130 or 45, and insurance, budget $600/month per vehicle.

-

The No-State-Income-Tax Benefit: Remember that while your property taxes are high, your "take-home" pay in Texas is roughly 5–8% higher than in states like California or New York. This extra cash flow is often what makes a $115k salary in Austin feel like $130k elsewhere.

The Strategy for 2026: The "Housemate" or "Suite" Hack

Many first-time buyers in 2026 who earn between $75,000 and $95,000 are getting into the market through House Hacking.

By purchasing a home with an ADU (Accessory Dwelling Unit) or a floor plan designed for a roommate, they are using $1,200/month in rental income to offset their mortgage. This effectively lowers their "Required Personal Income" by nearly $40,000, making a $450,000 home accessible on a $75,000 salary.

To buy a median-priced home in Austin in 2026, you need a household income of approximately $115,618. However, you can buy in emerging suburbs like Kyle or Buda with an income as low as $83,000, provided you have a clean debt-to-income ratio.