Published August 29, 2025

Why Buying Real Estate Is a Good Investment (With a $400K Case Study That Shows You Why)

If you’re wondering whether real estate is still a smart investment — especially in a market like Austin, Texas — you’re not alone.

With headlines about inflation, rising interest rates, and stock market volatility, many people are asking:

“Is now a good time to buy real estate?”

Here’s the simple answer:

Real estate remains one of the most powerful tools for building long-term wealth — especially when you understand how to leverage appreciation, tax strategy, and rental income.

In this article, we’ll show you:

-

Why real estate has long-term investment advantages

-

A real-life case study of a $400,000 investment property

-

How tax strategies like cost segregation and 1031 exchanges can multiply your returns

-

Why smart investors choose real estate over stocks, crypto, or savings accounts

Let’s dive in.

Why Real Estate Is Still One of the Best Investments You Can Make

When people think about investing, they often compare real estate to stocks or mutual funds. But real estate has some major advantages those options just can’t match:

Tangible Asset

You can touch it, see it, rent it out, and improve it. That makes real estate more stable than paper assets that rise and fall with market swings. Sometimes, uses of real estate can be changed or optimized.

Leverage

With just 20% down, you control 100% of the asset — meaning your returns compound faster than most other investments. You gain, for example, 4% appreciation on the entire value of the property - not just the cash portion you used to purchase it.

Appreciation

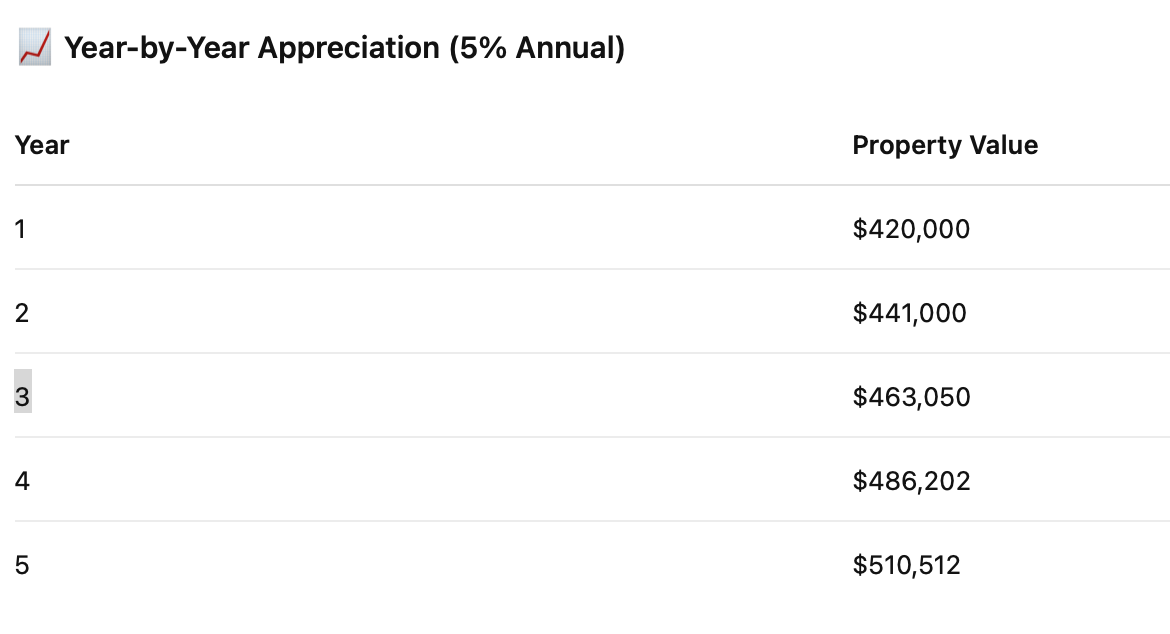

Home values tend to increase over time, especially in growing metro areas like Austin. Even a conservative 5% annual increase can lead to significant gains.

Tax Advantages

Depreciation, cost segregation, 1031 exchanges, mortgage interest deductions, capital improvements, maintenance and management fees, and more — these aren’t available to stock investors.

Cash Flow

You can collect monthly rental income while the asset appreciates and you pay down the mortgage.

Now, let’s walk through a real-world example to see how this plays out.

Real Estate Investment Case Study: $400,000 Property in Austin, TX

Let’s assume you purchase a $400,000 investment property in a desirable Austin suburb. You put 20% down ($80,000) and finance the remaining $320,000 at 7% interest over 30 years.

Key Assumptions:

-

Purchase price: $400,000

-

Down payment: $80,000 (20%)

-

Interest rate: 7%

-

Loan term: 30 years

-

Rent income: $2,800/month

-

Expenses: $900/month (taxes, insurance, maintenance)

-

Appreciation rate: 5% annually

-

Hold period: 5 years

-

Cost segregation depreciation: Accelerated over 5, 7, 15 years

-

Exit strategy: 1031 exchange into larger asset

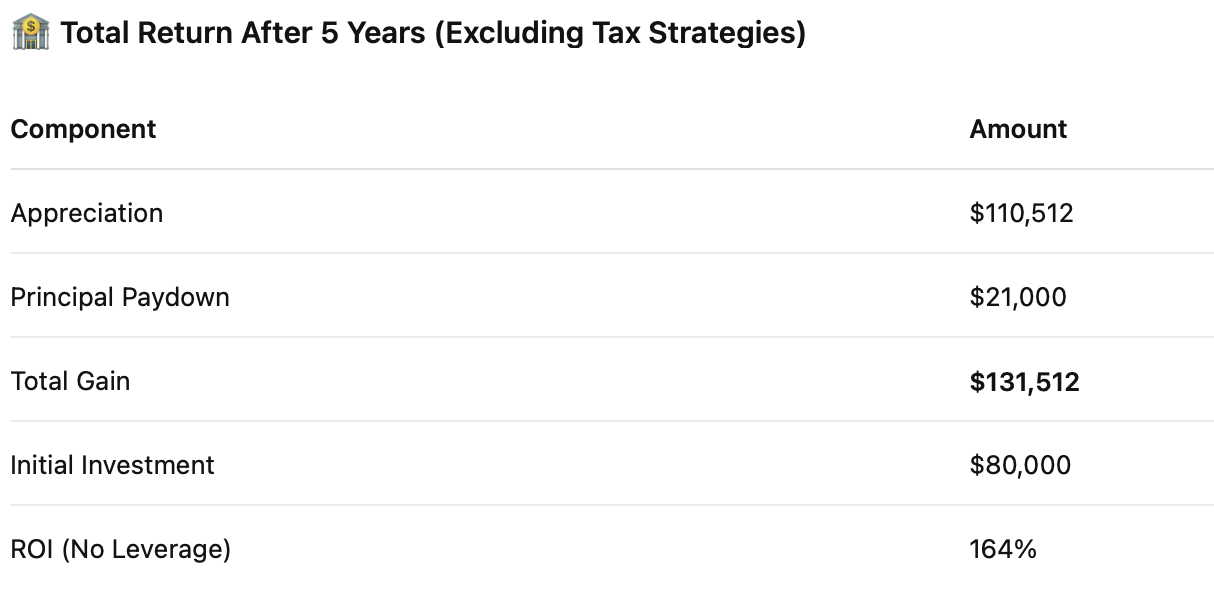

After 5 years, your $400K property is worth $510,512 — a $110K gain in value.

Cash Flow Over 5 Years

Let’s estimate a monthly cash flow:

-

Rental Income: $2,800

-

Mortgage (P&I): ~$2,129

-

Expenses: $900

-

Net Monthly Cash Flow: ~ -$229 (slightly negative cash flow at purchase)

But that doesn’t tell the full story — because your tenants are paying down your mortgage every month.

Principal Paydown Over 5 Years

Over 5 years, you’ll pay down roughly $21,000 of principal, which becomes equity.

Unlocking Extra Returns with Cost Segregation

Here’s where savvy investors unlock real wealth: cost segregation.

What Is It?

Cost segregation is a tax strategy that allows you to accelerate depreciation by separating personal property and land improvements from the building.

Instead of depreciating the whole property over 27.5 years (for residential), you can break parts down into:

-

5-year (appliances, carpets, cabinets)

-

7-year (fencing, outdoor lighting)

-

15-year (landscaping, driveways)

Real-World Impact

Let’s say a cost segregation study allows you to depreciate $90,000 in the first 5 years.

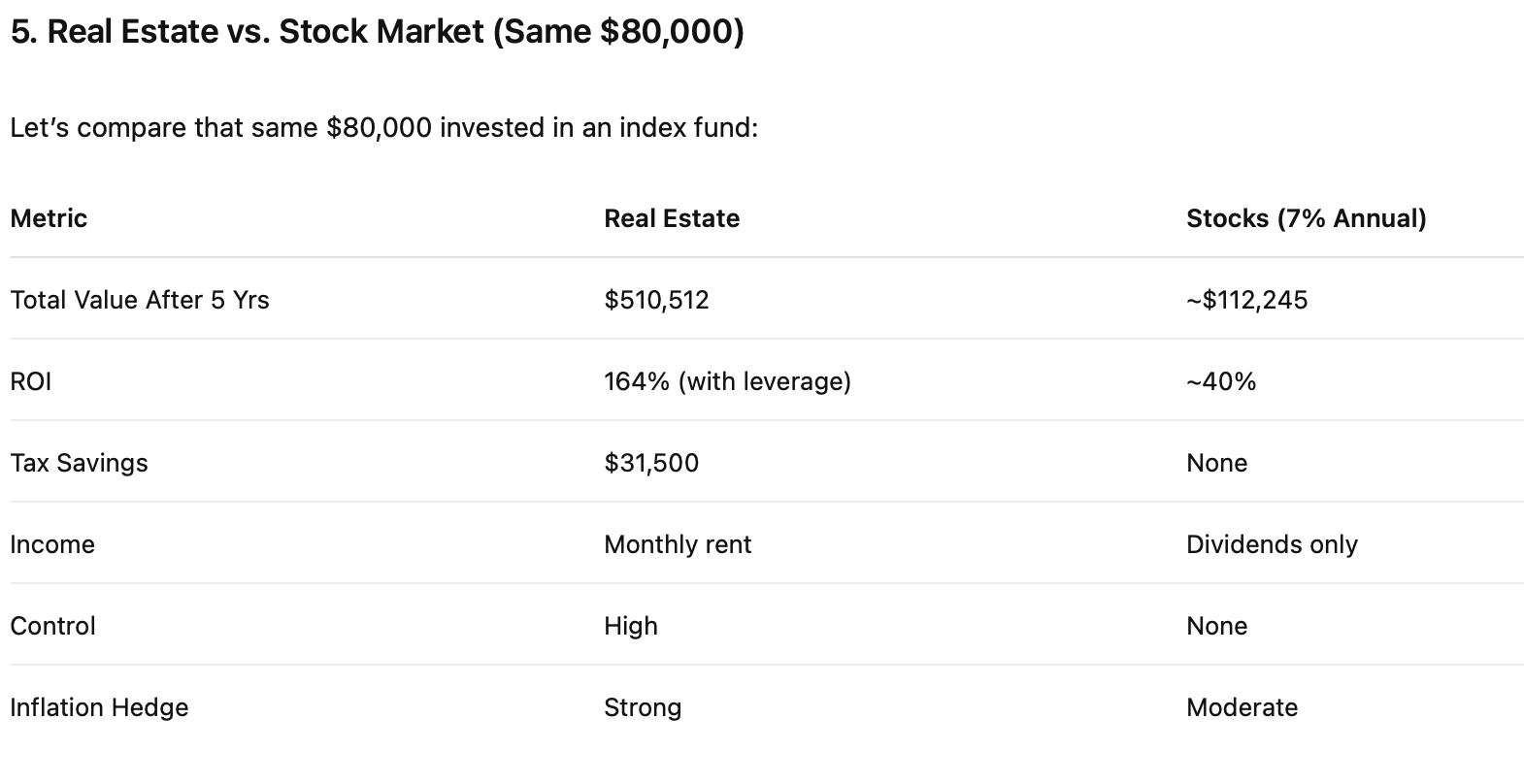

If you’re in a 35% combined tax bracket, that’s $31,500 in tax savings over 5 years — effectively increasing your cash-on-cash return without changing rent or appreciation.

That’s real money you keep in your pocket. This is a tax deferral strategy that is most often used effectively in years where investors earn a lot of money... and they want to offset the tax liability. The government will get their tax money when you sell the property through recapture. Unless...

Multiply Your Wealth with a 1031 Exchange

What if you don’t want to pay taxes when you sell?

Enter: The 1031 Exchange

A 1031 exchange lets you sell a property and roll all the profits into a new property — without paying capital gains taxes (as long as you meet the IRS criteria).

In our example:

-

You sell the $510,000 home

-

Roll the full proceeds (minus the mortgage) into a $650,000 duplex

-

You now own a more valuable asset that generates more income without losing 20–30% to taxes

Bonus: The Real Estate Wealth Ladder

This is how investors build real portfolios:

-

Buy a $400K house

-

Use cost segregation to reduce taxes

-

Let it appreciate

-

1031 exchange into a $650K duplex

-

Repeat until you own multi-million-dollar assets

Final Thoughts: Why Smart Investors Bet on Real Estate

The secret is out: Real estate is not just about owning “property” — it’s about owning opportunity.

You’re leveraging other people’s money (the bank and tenants), reducing your taxes, gaining appreciation, and building a financial future you control.

In a world of economic uncertainty, real estate gives you control, predictability, and multiple income streams.

Want to Learn More About Investing in Austin Real Estate?

At Byrne Real Estate Group, we help clients and investors buy smart, sell well, and use strategies like cost segregation, 1031 exchanges, and mortgage incentives through our in-house mortgage company — Buyer’s Rate Mortgage — to maximize their investment.

We’ll help you:

✅ Analyze the best properties

✅ Connect with tax and legal pros

✅ Structure your investment for long-term success

✅ Save thousands on financing and fees

------

Frequently Asked Questions (FAQ)

1. Is now a good time to invest in real estate, even with high interest rates?

Yes — especially if you’re buying in a strong market like Austin. While higher rates can reduce initial cash flow, they also create less competition and more negotiating power. Plus, real estate is a long-term game. You can refinance later when rates come down, but you can’t go back and buy today’s prices in tomorrow’s market.

2. How much money do I need to get started?

Most conventional investment loans require 20–25% down, so for a $400,000 property, you’d need $80,000–$100,000 plus some closing costs and reserves. However, creative options like partnering, HELOCs, or using your primary residence equity can help reduce the upfront burden. And once you’re in the game, you can use 1031 exchanges and appreciation to scale.

3. What is cost segregation, and how does it benefit me as an investor?

Cost segregation is a tax strategy that accelerates depreciation by breaking the property into components (like appliances, landscaping, and fixtures) with shorter life spans. Instead of deducting depreciation over 27.5 years, you get big deductions upfront — often saving $30K+ in taxes over five years on a $400K property. It requires a professional study, but the return on investment is often significant.

4. What is a 1031 exchange and how does it work?

A 1031 exchange allows you to sell one investment property and buy another of equal or greater value — without paying capital gains taxes at the time of sale. It’s a powerful strategy to grow your portfolio tax-deferred, but it has strict rules:

-

You must identify a new property within 45 days

-

Close within 180 days

-

Use a qualified intermediary

We recommend working with an agent and tax pro experienced in 1031s to get it right.

5. What if my rental property doesn’t cash flow immediately?

That’s normal in many fast-appreciating markets. Even if a property breaks even or slightly loses money monthly, you’re still building wealth through:

-

Appreciation (rising home values)

-

Equity (mortgage paydown)

-

Tax savings (depreciation)

This combination often leads to strong long-term ROI — even with neutral or slightly negative early cash flow.

6. How do I choose the right property to invest in?

Look for properties in growing areas with strong rental demand, near major employers, schools, or transportation hubs. Analyze:

-

Rent-to-price ratio

-

Job and population growth

-

Crime and school ratings

-

Future development plans

Work with a local agent (like our team at Byrne Real Estate Group) who understands both the market data and the investor mindset.

7. What are the biggest risks of real estate investing — and how can I protect myself?

Like any investment, real estate carries risk. Common risks include:

-

Market downturns

-

Tenant issues

-

Unexpected repairs

-

Interest rate hikes

You can protect yourself by:

-

Having adequate reserves

-

Vetting tenants carefully

-

Getting proper insurance

-

Buying in the right location

-

Planning for the long term

With the right strategy and support team, real estate remains one of the lowest-risk, highest-upside investments available.